The Mother of All Financial Bubbles

Guest post by Chris Martenson of Peak Prosperity

At PeakProsperity.com, we pride ourselves on providing fact-based insight to breaking-news important events. How do we get it right? By using a science-based approach grounded in observation, deduction and a healthy skepticism of what the "experts" in charge claim.

Fukushima: Within 72 hours of the Japan tsunami in 2011, we had analyzed the situation and concluded with high probability that three core meltdowns had occurred at the Fukushima nuclear plant. While it took years for officials to finally admit to the full extent of the crisis, history has validated our initial analysis.

Oroville Dam: When California's authorities suddenly reversed course and scrambled to evacuate nearly 200,000 residents living downstream of the Oroville dam, within an hour, we had released an analysis of the situation, explaining the critical differences among the primary spillway, the main dam, and the auxiliary spillway.

The main lesson from Oroville -- or Fukushima, or Katrina -- is that governments do a poor job of relating accurate information to their citizens when big threats are involved. Part of that is likely due to a desire to avoid stoking fear. Part probably due to politics and bureaucracy. And part probably due to plain old incompetence.

Simply put, the authorities do not share all the facts necessary for making informed decisions. Which brings us to one of the truly great risks we're facing today. One with much more destructive potential than a single failed dam but, like Oroville, one the authorities are desperate to keep us in the dark about.

The Mother of all Financial Bubbles

We are now living through the mother of all financial bubbles. We've been living with it so long now that we have to take three giant steps backwards to even detect its broad outlines.

As a reminder, a bubble exists when asset prices rise beyond what incomes can sustain. Florida swampland in the 1920’s, tech stocks in the late 1990s, or Toronto real estate today -- all are fine examples of this.

The U.S. government and the private banking cartel known as the Federal Reserve, in cahoots with a very compliant and complicit mainstream media, are doing everything in their vast and considerable power to convince us that we are living in a golden era of risk-free prosperity. And that tomorrow will be even better.

Now, regular readers of PeakProsperity.com's reports will know there's a mountain of evidence contracting this. But it's critical to understand that this is the same public perception management style as we've recently seen at Oroville: Deny, deny, deny... and then finally admit the obvious.

So let’s take those three giant steps backwards and see if we can spot the flaw in the ‘everything is awesome!’ meme that the Fed et al are trying to paint for everyone by flooding the “markets” with so much thin-air liquidity (between $150-$200 billion a month) that nobody has any clue what anything is truly worth anymore.

Giant Step Backwards #1: Infinite Growth is Impossible.

This is such an easy concept that I'm continually surprised at how poorly appreciated it is and how much resistance it receives when raised. But it works like this: the earth is a sphere and therefore has a defined surface area and a defined amount of resources available for use.

The availability of these resources ranges across a spectrum from dense/concentrated on one end to dilute/useless at the other. Humans have already extracted and consumed most of the easily obtainable stuff. Now it gets harder.

Regardless of the economics of these resources, they are finite. And as our economy requires resources to function, if we want our economy to grow from here, that means consuming more resources at a faster rate than we have been. If resources are finite, then growth will one day prove finite, too.

This should be utterly, blindingly obvious to everyone. But it’s not, apparently. The Federal Reserve and the central banks in other nations are unified in their call for more economic growth, always and forever. That’s plan A. There is no plan B.

Giant Step Backwards #2: You Can’t Print Your Way to Prosperity.

History is replete with the failed attempts of nations to print their way to prosperity. The pursuit operates on the same principle as alchemy: trying to get something for nothing. It has invariably and always ended the same way. In tears.

At first, issuing more currency feels good because those closest to the money printing get stinking rich while doing practically nothing. As that trickles down, everybody initially feel smart and wealthier. Well, not everybody; but those running the system sure do.

After a while, though, all that feel-good activity is revealed as a fraud. It turns out prosperity wasn't printed, instead it was redistributed. From one party’s pocket into another. And in most cases, from poorer pockets into those of the already-privileged.

The same is happening today with the "thin air" money printing being conducted by the world's central banks. We are now living with one of the most extreme wealth gaps in U.S. history, with the top 1% (really, the top 0.1%) owning a greater percentage of the nation's wealth than they ever have.

But it's even more nefarious than that, because the Fed is not simply stealing from today's public; it is also stealing the prosperity of future generations. When the party being stolen from hasn't been born yet, it can't fight back.

In short, you cannot print your way to prosperity. Yet somehow we've forgotten that. And we're dooming ourselves (and our children and grandchildren) to becoming serfs in the process.

Giant Step Backwards #3: You Can’t Grow Your Debts Faster Than Your Income Forever.

This, too, should be completely obvious. You know perfectly well it holds true for your personal life or your business, if you have one. And it’s equally true for a nation, which is simply an aggregation of individuals and businesses. But somehow this simple truth has been either forgotten or deliberately ignored by today's economists and politicians.

Our grand experiment in debt-based fiat currency -- unbacked by anything tangible, like gold -- began on August 15th, 1971 when Nixon unilaterally broke the Bretton Woods agreement and forced the entire world off of the gold standard. Not that the world minded much, because this then meant that politicians and monetary hacks everywhere could ignore centuries of economic lessons and begin making exorbitant promises by printing currency like mad.

The giant step towards monetary (and debt) expansion this represented is clear to anybody who can read a chart.

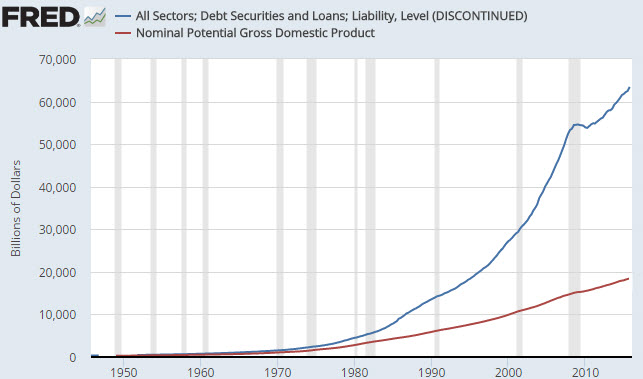

Here’s the total credit market debt in the U.S. It has exploded higher at a near-perfect exponential rate since that fateful day in 1971:

But what we really need to do is compare debt to income. Remember, you're not supposed to grow the former at faster rate than the latter. So let’s add (nominal) GDP to our chart and see what comes up:

As you can see, those lines began diverging a long time ago (aha! Right around 1971. Imagine that.). They've been diverging at an increasing pace for pretty much the entire adult lives of everybody in power. At this point, our leaders just assume “This is how the world works.”

“Reagan proved that deficits don’t matter” ~ Vice President Dick Cheney

The little wiggle in the exponential curve there, during 2008-2009, was the wiggle that almost destroyed the world. Our entire system of credit and money came very close to full-scale collapse, simply because it didn't grow for a few brief years. Makes you shudder to think what would have happened had it actually contracted...

But back to the main point. If we compare the beginning of this wanton debt-binge in 1970 with the state of things today:

We see that debt has shot up by a factor of 40 while income has only increased by a factor of 17. We have indeed grown our debts wildly faster than our income over the past 45 years.

And, it should be noted, a lot of that GDP ‘growth’ is the byproduct of borrowing and spending money we don’t have on things we don’t need. Said differently: the debts will remain during any serious future economic downturn, but the GDP that is fraudulently based on excessive rates of borrowing will vaporize as if it never existed in the first place.

That, my friends, right there is the very definition of unsustainable.

If something cannot go on, it won’t.

A Series of Unfortunate Decisions

How Did We Get Here?

Here’s my model for when where and how things went wrong, and why a series of Fed Chairmen from Greenspan, to Bernanke and now Yellen all shoulder some of the blame. Of course, all of their sycophant lackeys on the FOMC who voted with them time after time are culpable too. But the captain always bears ultimate responsibility.

Error #1: In 1994, facing a corporate bond mini-crisis, the Fed under Greenspan decided to eliminate bank reserve requirements via the nefarious 'sweeps' program.

This rule change allowed banks to create mirror accounts for each demand account (checking and/or savings) and 'sweep' money out of those demand accounts each night right before the stroke of midnight when the reserves 'snapshot' is taken. With nothing in those accounts at that moment (as they would have $0 balances) nothing needs to be held in reserve against them. Then, a few minutes later, the money is swept back in.

Problem solved. With banks now flooded with liquidity because they had vastly reduced reserve requirements, there was money sloshing everywhere looking for things to do. It sloshed right out into the tech bubble, which grew until it had spawned the sort of reckless behavior that gave us …

Error #2: The Long term Capital Management (LTCM) Fiasco of 1998 is when Greenspan stepped in and saved Wall Street from serious losses brought about by wildly reckless trading rooted in derivatives that blew up spectacularly. Instead of allowing those losses to be borne by the responsible parties, Greenspan bailed the whole mess out. While only measuring in the low billions, quaint by today’s numbers, this episode taught Wall Street two things:

- If you are going to blow up, blow up big because then the Fed will bail you out (a.k.a. ‘moral hazard’) and

- If you spin it right, everybody focuses on the losses of LTCM and forgets to ask who were the winners and why did they get to keep those winnings?

Indeed that’s exactly what happened and that planted the seeds for the even larger disaster that was to follow in the sub-prime housing crisis less than ten years later. Lessons learned.

By Wall Street that is, not the Fed. They blundered even further by making…

Error #3: Lowing Interest Rates to 1%. Instead of simply taking the lumps of crappy, sub-par growth as the nation worked off the prior two errors and debt binges, Greenspan decided to throw more money to Wall Street via ultra-low interest rates.

All this did was fuel a major housing bubble which then burst. But it could not and would not have been as bad, or even happened at all, if (a) Wall Street wasn’t encouraged to take stupidly huge risks with untested CDO derivatives secure in the knowledge that they’d be bailed out again and (b) interest rates had not been unnaturally jammed to such low levels.

Adding to it all was a highly complicit main stream media that breathlessly told tales of house flipping riches and Fed researchers who cranked out supporting studies proving there was no housing bubble. But burst it all did which brings us to …

Error #4: Repeating the Same Low Interest Rate Mistake. Displaying that the Fed truly has a flat learning curve, Bernanke decided it was his job to have “the courage to act” (the title of his overly self-important memoirs) and save the country by holding another low interest rate blow out special. Apparently, the spectacle of Wall Street greed and the deeply unfair practices of seeing them bailed out could not dissuade Bernanke from being courageous by giving Wall Street another go.

Only this time with extra sauce. Not content with merely low rates, Bernanke decided to ‘turn Japanese’ and commit to trillions of Quantitative Easing (QE)…which is nothing more than shoveling money straight into the Wall Street furnace. Main Street continued to suffer, while Bernanke went to cocktail parties where thrilled bankers and billionaires feted his courage.

After all, it takes a brave man to brazenly loot his country for the few at the expense of the many and the future.

Error #5: Doubling Down on QE. If the Fed felt compelled to act in the face of an emergency (of its own making let us belabor) then by late 2011 it should have been entirely clear that emergencies don’t last more than a year. If they do, you are facing something structural. Not an emergency. But something else.

That would have been a great time to reflect and reconsider. But, nope, not the Fed. The doubled down and recommitment to the largest central bank balance sheet expansion in all of history. They blew bubbles across the globe. They enriched the already too-wealthy of the world. They fixed nothing and did all of this while consciously and knowingly ruining pensions, and savers (threw granny under the bus), and preventing millennials from having any shot at starting a household (by stealing interest income from their parents and ramming house prices back up via low interest rate policies).

Janet Yellen picked up the Baton from Bernanke and basically screwed over the young and the working classes in her quest to secure ever higher wealth gaps for her friends and even larger profits for the big banks.

Worse, all this bad behavior then spread across the globe with Japan and Europe following suit. If you want to understand Trump and Marine Le Pen, you need to understand errors #4 and #5. They did not come out of nowhere, they came from deeply unfair monetary policies with the U.S. decidedly leading the way.

Error #6: Preventing a Market Decline. In January 2016, the world markets were in disarray. For those inclined to read charts look at the third giant top that formed there throughout 2015 and into 2016. It is as clear a mega top as you could hope to see. What should have happened there was a reasonable market decline. But suddenly, out of nowhere, massive buying arrives and drove the market higher. I have no doubts in my mind that central banks were behind that, and I‘d love a full audit to check that theory.

Then things got dicey with the Brexit vote a couple of months later and, again, a very puzzling, and counter intuitive blast of buying accompanied that vote…only this time a few hours afterwards. Then Trump won and, again, instead of being a black swan type moments of uncertainty, a massive wall of buying arrives only this time within hours of the win, arriving by 2:30 a.m. that Wednesday morning after that fateful Tuesday election.

Here we have the central banks desperately afraid of the Franken-markets they’ve created, locked into a desperate cycle of rescuing the “markets” to ever higher levels, not allowing them to ever correct.

Well, let me cut to the chase. You know what happens when markets are fiddled with in this way? They eventually crash, and crash hard.

The Big Reset

Let me be clear. The coming reset is going to be very, very painful. Part of me just wants to rip the proverbial Band-Aid off and get on with it, yet part of me dreads what’s coming and is in no hurry to see it arrive. Talk about being ambivalent!

You will not read about the coming reset in the New York Times. Or the Wall Street journal. Or hear about it from any Congressperson or Senator. You will not hear about it on the news.

I can fully guarantee you that smart people all over the place are now preparing for that reset. I know this because I talk to them personally.

Ex-military people are some of my favorites to talk to because they have no illusions. Risks have to be faced regardless of your desire to not face them or your belief systems. You either know what you are up against or you are unprepared and likely to be harmed. Special Forces operators also have the luxury of knowing intimately that what you read in the newspapers is pretty much complete hogwash. That’s a distinct advantage.

Economists and techno-fantasists are my least favorite people to talk to. They are rooted in beliefs that have no attachment to context. There’s no basis for a conversation that can go anywhere or provide anything useful to my life except for a renewed sense of how dangerously unprepared many people are for any future but the one in their heads.

So what will happen when the reset comes?

Look, I don’t have a crystal ball. So I’m just guessing here. But it seems that, given just how dangerously extended everything is, that we should expect major financial market disruptions.

I am personally planning for banks being closed, stock markets closed, funds gated, and capital control imposed. And that’s just for starters. If we can just get away with some destroyed banks and ruined fantasy wealth along with less global money movement, I’ll count that as a ‘win’ here.

So everyone should always be prepared to safeguard their money. Have cash out of the bank and, for heaven’s sake, have your money managed by competent professionals who understand the risks!

If we’d dealt with the structural issues back in 1994, then we could have gotten away with some pain, maybe a lot, but I truly think it would have been survivable. Now? Well, instead of falling off a 6 foot step-ladder, we’re now 40 feet up an extension ladder with one foot on the top rung and the other off to the side waving about for balance.

What if things get worse than a simple financial melt-down?

Well here we have to confront the possibility of far worse disruptions which could include severe social unrest. People are already angry after years of being trampled by self-dealing financial parties, with the Fed at the helm the entire way. Shame on them, by the way. Without knowing where the shocks are originating, people are increasingly (and inappropriately) turning against each other, in what we call The Fight Cage syndrome.

How many hours after people’s subsistence food and assistance cards from the government ‘go dark’ do you think it will be before the first riots? Hours? A day? Three days?

Once social unrest starts, how many hours or days do you think pass before the food stores are all stripped bare? How long after that will it be before the electricity goes away?

If any of this gets rolling, how long will it be before the government decides the right way out of this is to manufacture some reason to blame all this on an external enemy and declare war?

These are the worries, and they are not at all unthinkable or irrational.

But they are also all fear-based, and I am increasingly finding myself angry that I even have to be in this position at all.

Conclusion

The way forward, true solutions, require a new story, one that is not based on scarcity, and fighting and fear and dark actors with bad aims. We need to bring truth and beauty and poetry back into the mix.

We’ve lost out way as a nation and as a global people, and the root of all that is our system of money which quite bizarrely, has delivered us to the place where 8 people have as much wealth as 3.6 billion, and people report being scared about not having enough in the most abundant conditions in all of human history.

Part of that fear, though, is centered on the knowledge that we are quite rapidly destroying the planet and that feels awful.

So given the many mistakes of the past, and given where we are in the story, your first call to action is to secure your own place and your own future by becoming as resilient as you can.

Your next call to action after that is well underway is to begin helping to shape the new narrative. One based on love, respect, honor, dignity, meaning and authentic purpose. Unfortunately, the die is already cast. It has left the hand and now we are left to fate to see how it lands.

We cannot undo the many unfortunate decision of the Fed, but we can assure that we are living as joyfully and as resiliently as we can, with a keen eye to our role in shaping what comes next.